Life has a way of throwing curveballs when we least expect them. Job loss, sudden medical bills, unexpected car repairs, or even an unplanned move can create financial stress if you don’t have money set aside. That’s where an emergency fund becomes one of the most powerful financial tools in your toolkit. It is not just a safety net; it’s a financial shield that gives you peace of mind and the freedom to handle the unexpected without derailing your long-term goals.

Why an Emergency Fund Matters

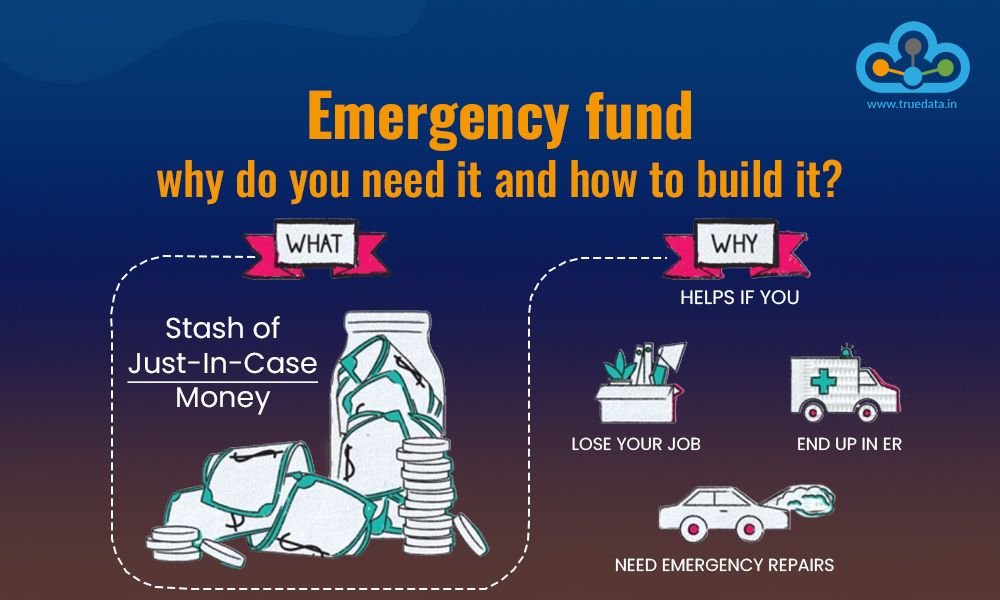

An emergency fund is money set aside specifically to cover unexpected expenses or financial shocks. Unlike investments or retirement accounts, it’s not about earning returns—it’s about liquidity, accessibility, and security.

Without such a fund, many people turn to high-interest credit cards or loans when emergencies strike. This creates a cycle of debt that can take months or even years to escape. By contrast, an emergency fund provides immediate cash that you can access without penalties or interest, ensuring that one crisis doesn’t spiral into a long-term financial setback.

There’s also a psychological benefit. Knowing you have money set aside brings financial confidence and reduces stress during difficult times. Instead of panicking about how to pay for an unexpected medical bill or a broken furnace, you know you already have a plan in place.

How Much Should You Save?

The golden rule financial advisers often recommend is saving three to six months of living expenses. This means if your monthly budget for essentials like rent or mortgage, groceries, utilities, transportation, and insurance comes to $3,000, your emergency fund target should fall between $9,000 and $18,000.

That said, the right number varies depending on individual circumstances. A single person with a stable job might need less than a family of four relying on a single income. Similarly, someone with variable freelance income or a business owner may want to aim for a higher cushion—perhaps even 9 to 12 months of expenses.

The calculation should always be based on “needs” rather than “wants.” Your emergency fund is meant to cover essentials, not luxuries, so focus on the expenses that keep your household running.

Where to Keep Your Emergency Fund

Accessibility is key. The money should be kept in a safe, liquid account where you can withdraw it quickly when needed. Popular options include:

- High-yield savings accounts – They offer better interest rates than regular savings accounts while keeping your money easily accessible.

- Money market accounts – Another safe option with limited check-writing privileges and competitive interest rates.

- Certificates of Deposit (CDs) with laddering strategies – Useful if you want a portion of your fund to earn higher interest, though you should always keep part of it immediately accessible.

Avoid locking away your emergency fund in retirement accounts, stocks, or long-term investments. While those are great for building wealth, they come with risks, penalties, or market volatility that make them unsuitable for emergencies.

Building the Fund Gradually

For many, saving several months’ worth of expenses may sound overwhelming. The key is to start small and stay consistent. Even setting aside $50 or $100 per paycheck will eventually add up. Automating transfers into a dedicated emergency account ensures discipline and reduces the temptation to spend the money elsewhere.

A useful milestone is to first aim for $1,000 in quick savings, which can cover minor emergencies like car repairs or medical co-pays. From there, steadily grow the fund toward the three-to-six-month benchmark.

Sample Savings Roadmap

Here’s a simple roadmap showing how someone saving $500 per month can build an emergency fund over time:

| Month | Contribution | Cumulative Savings | Equivalent Coverage |

|---|---|---|---|

| 1 | $500 | $500 | Covers small car repair or medical bill |

| 3 | $1,500 | $1,500 | Covers rent + utilities for one month |

| 6 | $3,000 | $3,000 | One month of living expenses |

| 12 | $6,000 | $6,000 | Two months of living expenses |

| 18 | $9,000 | $9,000 | Three months of living expenses |

| 36 | $18,000 | $18,000 | Six months of living expenses |

This roadmap can be adjusted depending on your income and savings capacity. The important thing is progress—every dollar you set aside increases your security.

When to Use the Emergency Fund

It’s important to define what qualifies as a true emergency. A shopping sale or vacation does not justify dipping into this account. Genuine emergencies include:

- Medical expenses not covered by insurance

- Job loss or reduced working hours

- Unexpected home or car repairs

- Essential travel for family emergencies

Being disciplined about usage ensures your fund remains intact when you need it most.

Rebuilding After Use

Using your emergency fund is not a failure—it’s the very reason it exists. But once you withdraw money, prioritize replenishing it as soon as possible. Adjust your budget temporarily, cut non-essential expenses, or redirect bonuses and tax refunds to restore the fund’s balance.

The Long-Term Benefits

An emergency fund goes beyond just covering unexpected bills. It supports smarter financial decisions across the board. For example, it gives you breathing room to job hunt without desperation, to decline predatory loans, and to avoid liquidating long-term investments at the wrong time. It also enhances your overall financial stability, making other goals like investing, retirement planning, or homeownership more achievable.

Conclusion

Emergency fund planning is not about preparing for “if” but for “when.” Life’s uncertainties are inevitable, but financial chaos doesn’t have to be. By steadily building a fund equal to several months of essential expenses, storing it in a safe and accessible account, and using it wisely, you create a buffer that shields you from debt traps and financial stress.